States Perform Differently as Inflation and Interest Rates Rise

While the economy in the United States continues to grow, the effects from rising inflation and elevated interest rates are showing up in various degrees across the nation’s 50 states and the District of Columbia.

States economies depend on some industries more than others and are consequentially performing differently. High-growth states, such as those across the Sunbelt, tend to be more sensitive to the rise in construction costs due to the amount of housing and infrastructure needed to support growth. In states with a large concentration of tech firms, such as California, Seattle and New York, higher interest rates have made tech firms more sensitive to profitability and affected payrolls. States dependent on energy, including Texas, Louisiana, Alaska and North Dakota are continuously affected by energy prices, which have been rising recently. Meanwhile, tourism remains below pre-pandemic levels in terms of international and group travelers, affecting Hawaii and Florida more than others.

This week, we examine how a series of economic indicators have fared at the state level across the nation.

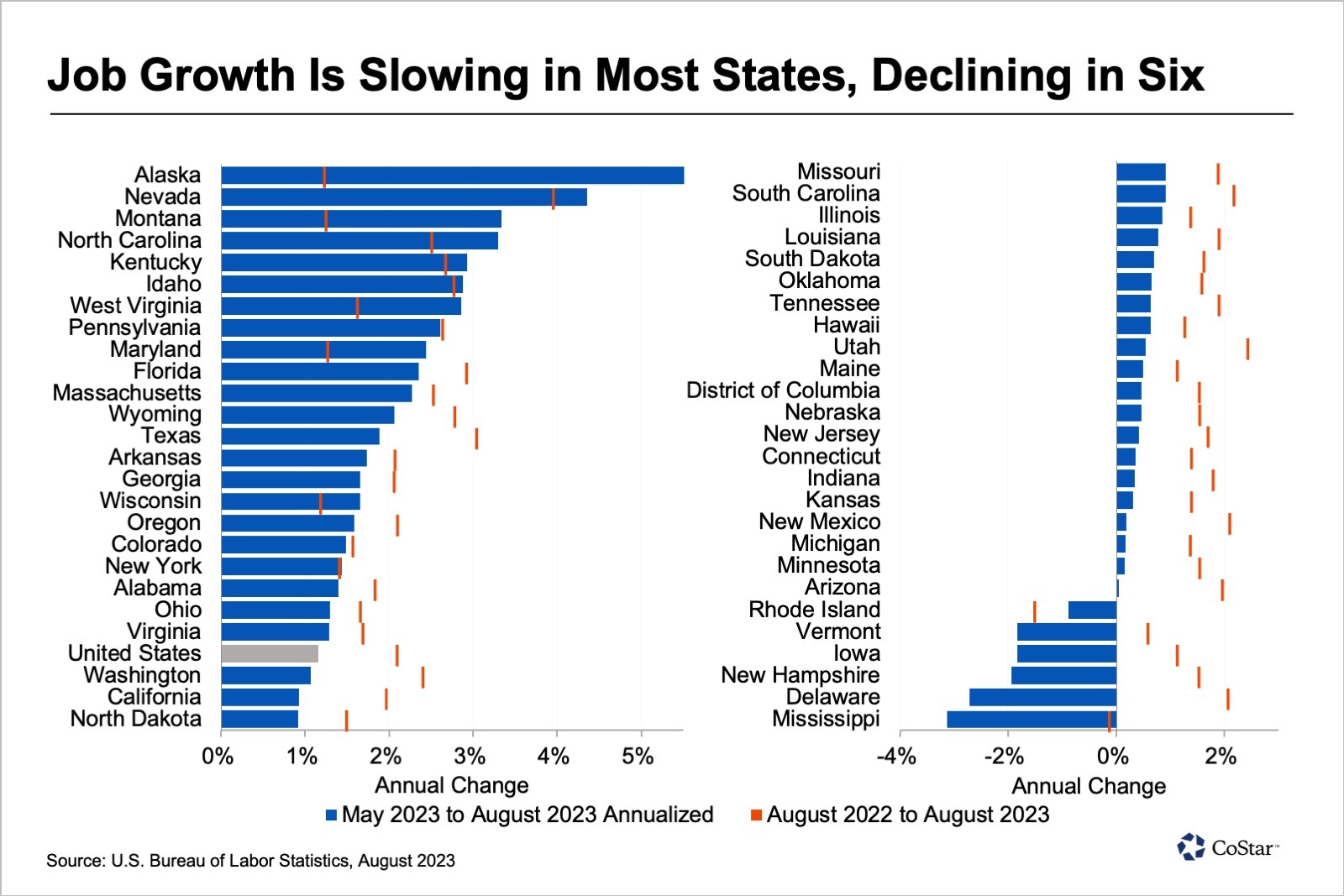

Nonfarm Employment: A handful of states in the West, including Alaska, Nevada, and Montana, have led job growth during the past three months, for some marking a reversal of job gains over the 12-month period. The three states, as well as Florida, have benefited from increased tourism, as a large proportion of job gains were in the leisure and hospitality sector. Some of these states have also benefited from the long-term tailwind in population growth.

Six states experienced job losses from May to August, most of which are located in the Northeast. Mississippi has been one of the few states in the South with population losses year after year. Job losses during the past three months have offset the modest gains during the previous nine months.

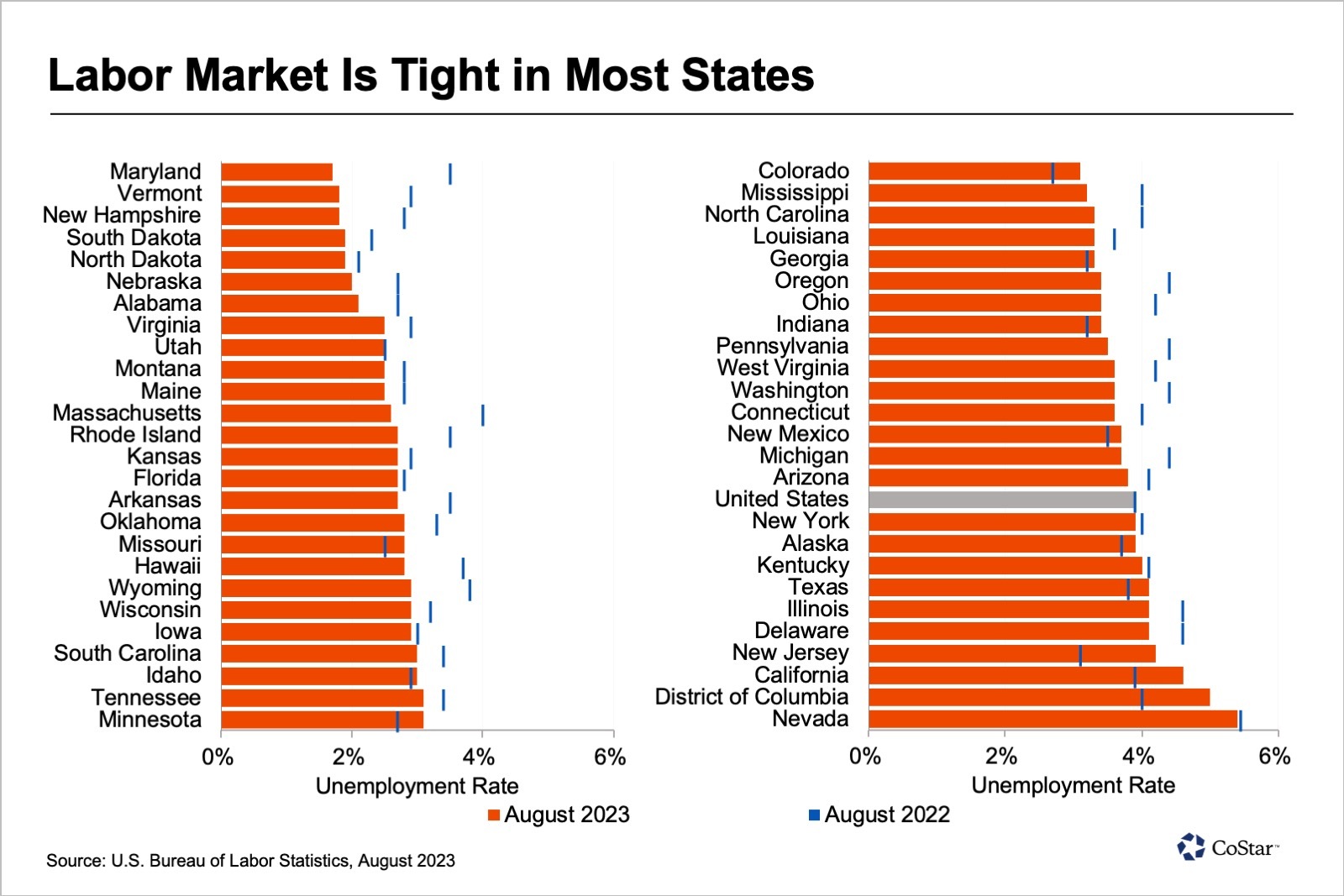

Unemployment Rate: While Nevada has been one of the leaders in job growth recently, it continues to have the highest unemployment rate in the nation. Elsewhere, labor markets are still tight, but they are loosening in many areas, including the District of Columbia, California, and New Jersey. Among other factors, these three places have higher minimum wages than the federal minimum wage of $7.25 per hour, ranging from approximately $14 to $16 per hour. Fast food workers in California are set to earn a minimum wage of $20 starting next April.

Some states with the lowest unemployment rates also have minimum wage ordinances, including Vermont and Maryland, but they are smaller states with a larger proportion of college graduates who tend to earn more than minimum wage.

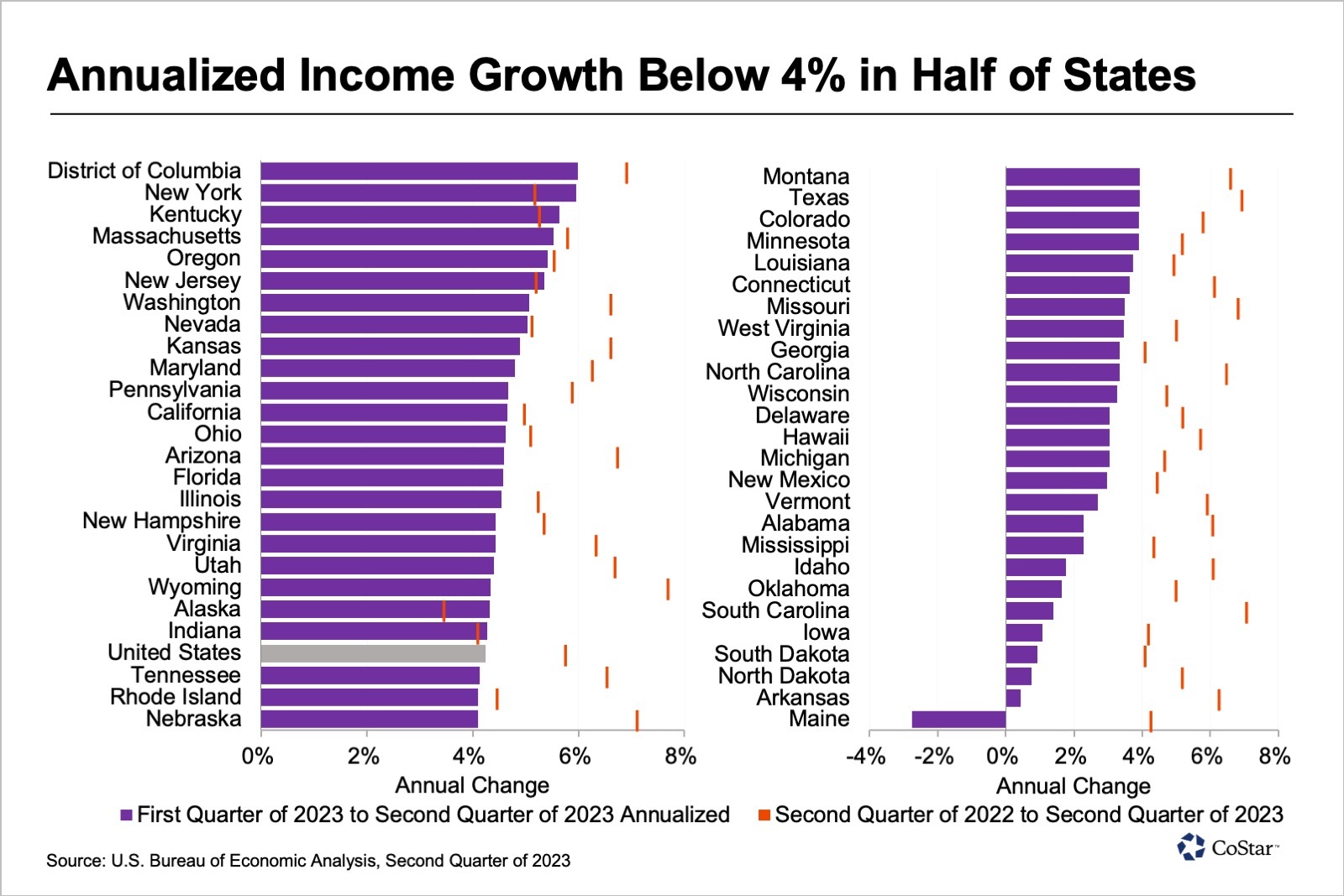

Personal Income: Income growth decelerated in most states during the second quarter of 2023 relative to the year-over-year change. Among the locales with the highest personal income growth during the quarter were those with a large concentration of financial services firms, such as the District of Columbia, New York, Massachusetts, and New Jersey. Firms in the sector benefited from a 13% increase in the broad S&P 500 stock index and a 21% increase in the tech-heavy Nasdaq Composite index.

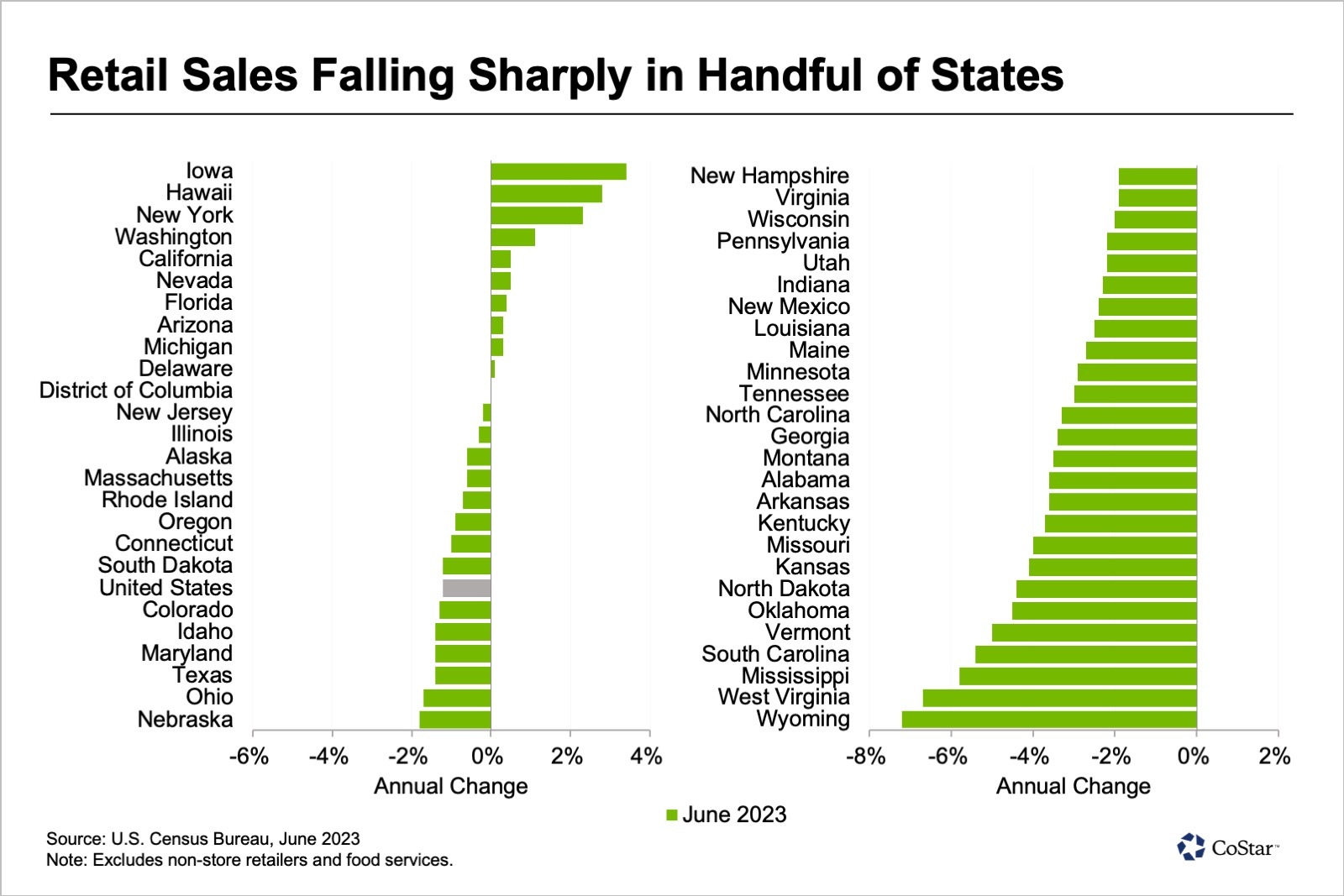

Retail Sales: Consumer spending has helped carry the economy, but shoppers have been pulling back in some states more than others. The Census Bureau recently introduced experimental data to help analyze retail sales at a state level, excluding non-store retailers and food services, both of which have been growing. In June, most states had year-over-year declines, with Iowa, Hawaii, and New York being notable exceptions. Some states that tend to benefit from being the most affordable for housing are experiencing the steepest decline in retail sales, including Wyoming, West Virginia, and Mississippi. In contrast, residents of higher cost-of-living states have benefited from long-term equity gains to help support spending.

What We’re Watching…

We’re awaiting September’s jobs report, which is scheduled to be released at the end of the week.

Job growth has been slowing over the year but still remains quite solid, with the three-month average of job gains at about 150,000. This is still higher than what the Federal Reserve would like to see, and expectations are that the data for September will come in softer. But a report from the Labor Department this week came as a shock, showing a jump in job listings and suggesting that the hiring market is still pretty healthy.

It’s helpful to note that this data comes from a survey that has seen response rates fall from around 65% in pre-pandemic days to just about 32% today on initial release, so we’re leaving a lot of data on the cutting floor, so to speak. The jobs report, on the other hand, uses an establishment survey that has consistently had response rates in the 70% range on initial release, and its final release is in the mid-90s.

We follow revisions to the jobs report quite closely, but rarely report revisions in data on job listings.