Small Business Checkpoint: Profits Growing, Jobs slowing

Key takeaways

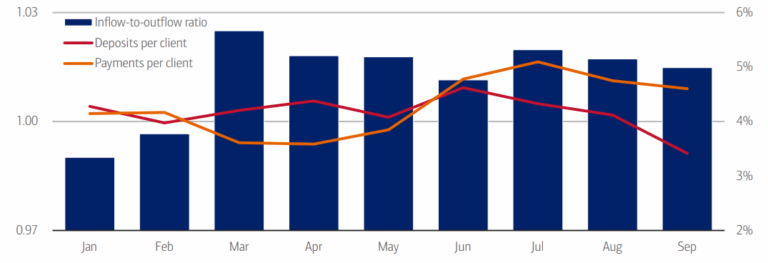

• Our measure of profitability for small businesses, the inflow-to-outflow ratio, held at 1.01 in September. However, moderating

deposit growth per small business client could be a sign of weaker revenue growth for small firms as payment growth outpaces,

according to Bank of America small business account data.

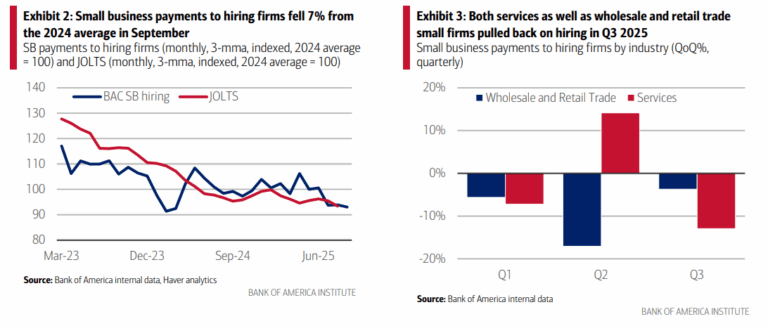

• Meanwhile, Bank of America’s small business alternative hiring indicator dropped 7% in September from the 2024 average, with

an even sharper drop of 12.9% quarter-over-quarter for services firms. Furthermore, business applications with planned wages –

often a signal of real job creation – have dropped below pre-pandemic norms, pointing to labor market softness.

• Credit card balances per small business client rose by 3% in September vs the 2024 average, faster than the utilization rate,

suggesting some firms are carrying debt forward. Even so, tightening of lending standards from banks has eased, with fewer

banks reporting stricter lending to small firms than large ones, indicating that credit access remains relatively resilient.

Small business profits still up

Despite small business uncertainty reaching the fourth-highest reading in over 51 years, 1 in September, small business profits were still positive according to Bank of America small business account data, with the inflow-to-outflow ratio at 1.01 (Exhibit 1).

Though this is down from both the March peak and August, it signals some cushion for small firms, with profitability growth up 0.1% year-over-year (YoY) on a three-month moving average (3-mma).

But what’s driving the underlying trend for positive profits – fewer costs or higher revenue? Bank of America deposit growth per small business client suggests the answer is the latter. However, revenue has trended downwards since June, though remains positive, which might suggest weaker revenue growth for small firms going forward.

This is further supported by the September National Federation of Independent Business (NFIB) report, which found that while most owners evaluate their own business as currently healthy, they are having to manage rising inflationary pressures, slower sales expectations, and ongoing labor market challenges.2

Small business labor market is slowing

Notably, there are further signs of a slowdown in the small business labor market. Our proprietary alternative hiring indicator based on Bank of America small business (SB) payments data (see Methodology below) was down 7% in September (Exhibit 2).

This is consistent with the narrative of hiring deceleration presented in the Job Openings and Labor Turnover Survey (JOLTS) August reading.

For small services firms, hiring was down 12.9% quarter-over-quarter (QoQ), reversing the gains from the previous quarter (Exhibit 3), which may have been reflective of some seasonal summer hiring. Additionally, wholesale and retail trade – both sectors more exposed to tariffs – have continued to pull back on hiring, though there was slight improvement from Q2.