C&W U.S. Office Reports for Quarter 2 of 2024

Key Takeaways For Q2 2024

- The U.S. economy is slowing but continues to be remarkably resilient. Real GDP decelerated from an unsustainable 3.4% rate of growth in Q4 2023 to 1.3% in Q1 20241 and is tracking at a similar rate of growth for Q2 (in the 1.5% range). Job growth also moderated in Q2 but remains healthy.

- Office demand came in negative for the tenth quarter in a row. National absorption was better than last quarter, but still came in at -18.2 million square feet (msf). Second quarter absorption was positive, however, in a third of U.S. office markets.

- Construction activity keeps declining. With 17.7 msf delivered in the first half of the year, office deliveries are 27% below the average since 2020. The current pipeline is now down to 44.3 msf—its lowest point in over a decade.

- The quality bias continues. Occupier demand continues to favor buildings of the very highest quality. Office occupancy of these assets in gateway markets2 remains 750 bps higher than the overall office average. Existing high-quality assets will continue to outperform as this highly sought after space will face less competition given the sharp falloff of new construction.

Economy Is Slowing but Still Creating Jobs

The overall job market has remained resilient thus far in 2024, but not uniformly across sectors. Nonfarm payrolls are up 1.7% year-over-year (YOY) as of June, which is in-line with the first quarter of 2024 but below the 2.0% growth rate for 2023. Healthcare and education (+4.2% YOY), government (+2.7%) and leisure and hospitality (+2.0%) continue to be leading growth sectors. Office-using employment also continues to grow, but at a slower rate. In the first half of this year, the U.S. economy added 192,000 office-using jobs (excluding temporary workers), down from 246,000 in the first half of 2023.3 Given that the U.S. economy is now slowing, we expect office-using job growth to moderate for the remainder of the year before picking up in 2025 as the economy re-accelerates.

Positive Absorption in a Third of U.S. Markets, but National Demand Remains Negative

For the tenth quarter in a row, national absorption was negative. With -18.2 msf of net negative absorption in the second quarter, the four-quarter rolling total was -69.6 msf. Although still negative, Q2 was an improvement from the -25.5 msf observed in the prior quarter.

On the bright side, over half of U.S. office markets (50 of the 93 tracked by Cushman & Wakefield Research) saw improvements quarter-over-quarter (QOQ). Twenty-eight markets have experienced positive absorption for the first half of the year, including eight markets where H1 absorption totals exceeded 200,000 sf: Puget Sound – Eastside (+828,000 sf), New Haven, (+578,000 sf), Baltimore (+444,000 sf), Nashville (+362,000 sf), Memphis (+361,000 sf), Tampa (+264,000 sf), Oklahoma City (+259,000 sf), Birmingham (+233,000 sf) and Austin (+225,000 sf).

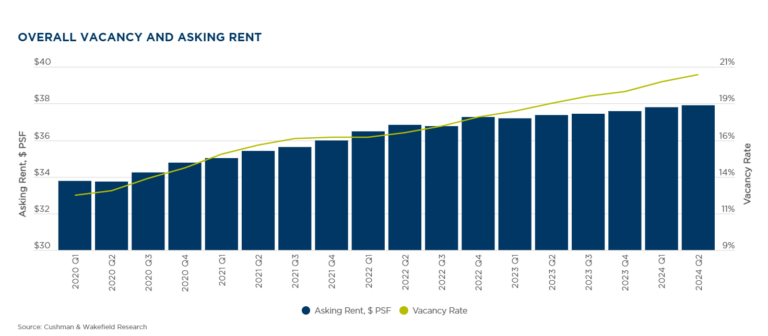

National vacancy ended the second quarter at 20.5%, a record high, up 55 basis points (bps) QOQ and 180 bps YOY. The vacancy rate has increased by 785 bps since the beginning of the pandemic. This is a greater increase than in the wake of the Great Financial Crisis (+470 bps from 2007-2010) but still well below the Dot-Com increase (+915 bps from 2000-2003).

New Office Supply Declines to Decade Low

Commercial real estate pipelines have been declining for all property types (including office, industrial and multifamily) due to high construction costs, market fundamentals and the high cost of capital in the current interest rate environment. The office sector, of course, has substantial headwinds related to softness in the market and the uncertainty of when demand will solidify.

Office deliveries have receded from recent highs, and 2024 is currently on track to see the lowest amount of new deliveries in the U.S. since 2014. In the first half of the year, 17.7 msf of new office space was delivered in the 93 U.S. office markets tracked by Cushman & Wakefield, which is 27% below the H1 average over the past five years (24.2 msf). New deliveries added just 0.3% to overall office inventory in the past six months.

Moving forward, construction activity is likely to dissipate even further. Our U.S. Outlook calls for deliveries to get below 10 msf per year—less than one-fourth the 10-year historical average of 47 msf per year. The current national pipeline is at 44.3 msf, the lowest level since Q4 2012. The pipeline is down 67% from the Q1 2020 peak of 135 msf. The Q2 2024 construction pipeline is the equivalent of 0.8% of current U.S. office inventory, just a third of what it was in early 2020 (2.5%) and half of the 10-year pre-pandemic average (1.5%). The strongest demand has been for new and high-quality space. The shrinking pipeline suggests the market will soon be underbuilding the space occupiers want most, but lower delivery totals should help the broader market recover, giving existing buildings time to stabilize occupancy with less competition from new construction.

The increase in sublease space is also slowing down as the amount of office space available for sublease increased 1.0% QOQ, reaching 153.4 msf in Q2. The YOY increase of 4.3% is the slowest pace recorded since the Federal Reserve started increasing interest rates in March 2022 and the second slowest YOY increase since the end of 2019. Sublease availabilities are down YOY in half of U.S. markets, with declines in gateway and gateway-adjacent markets such as Baltimore, Fairfield County, Central NJ, Northern VA, Oakland/East Bay, San Francisco North Bay, Suburban MD, Washington, DC and Westchester County.

For the data behind the commentary, download the full Q2 2024 U.S. Office Report.